Sample project

How does the mortgage interest deduction in the US affect the proportion of homeowners and the property markets?

One of the most widespread incentives for homeownership is the mortgage interest deduction. The effects of these subsidies on the US federal income tax revenue are significant. In the United States, the mortgage deduction amounts to 100$ billion loss in potential tax revenue.

Although these tax incentives create increased demand for homeownership, the effectiveness is controversial. First, the supply of housing in urban areas is scarce and can only be increased at considerable costs. Accordingly, the increased demand in cities leads to higher house prices without resulting in more homeowners. Second, these tax benefits are regressive because wealthy households have higher tax deductions since they own disproportionately more expensive houses. Third, the tax incentives apply to all homeowners, even though they do not influence the tenure decision at a certain income level.

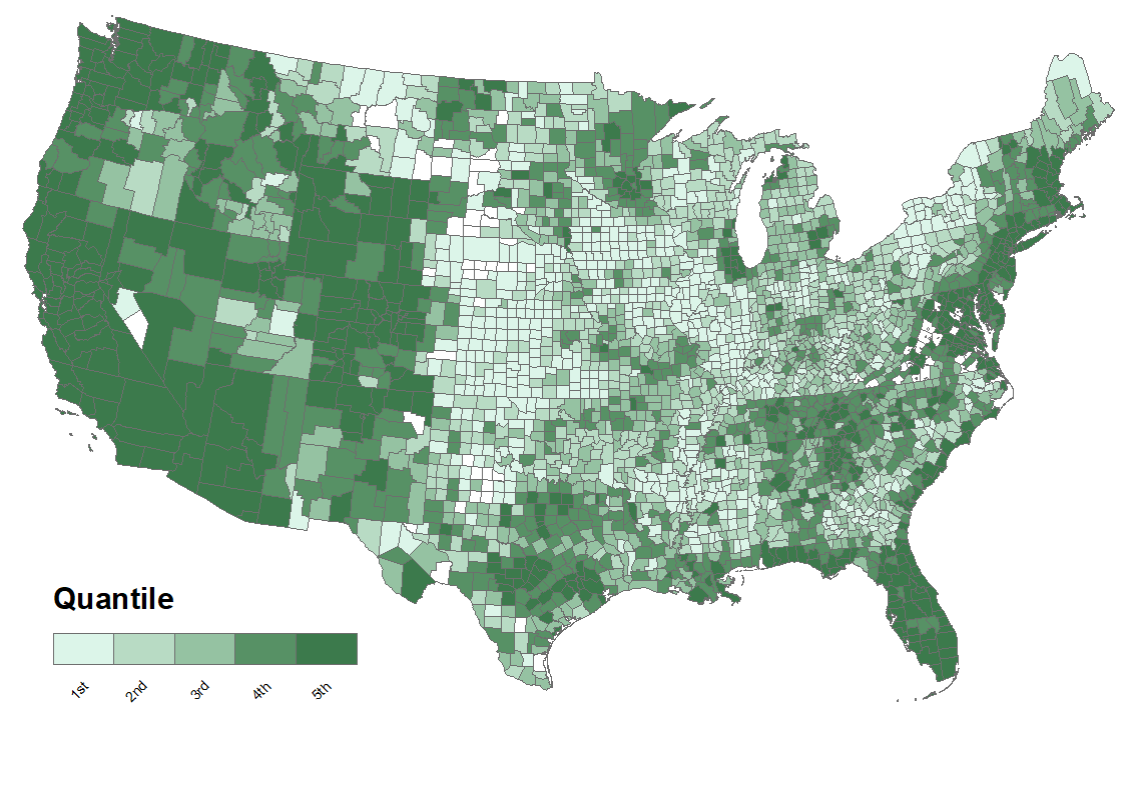

Figure 1: Average mortgage interest deduction subsidies per homeowner. Dark green regions have the highest subsidies.

Figure 1: Average mortgage interest deduction subsidies per homeowner. Dark green regions have the highest subsidies.

In a current research project on the US, we use a spatial equilibrium model to investigate the effectiveness of the mortgage interest deduction on homeownership and the real estate markets. Although all households have the same tax deduction options, this measure is particularly effective in areas with large undeveloped areas with lax land-use regulations. According to our analysis, the mortgage interest deduction in the US leads to an increase in house prices in urban regions with a restricted housing market. In these regions, the proportion of homeowners in the population increases only slightly or even declines. The mortgage interest deduction shifts the population from urban to rural areas and also leads to an increase in commuter flows. Overall, the increase in homeownership compared to potential tax losses is small.